"If you can speak what you will never hear,

if you can write what you will never read,

you have done rare things."

-Henry David Thoreau

"Doctor, how much longer?"

The case had gone smoothly, but the challenges of mapping the infrequent skipped beats that signified the initiating sequence to the tachycardia was getting more difficult. "Could it be left sided?" I wondered. "Anterior or posterior? I've tried the posterolateral area and that timing was late. Clearly anteromedial was earlier. All the darn beats look so similar with pace-mapping."

I had been working for an hour and a half without effect when I had an idea: "Maybe the 3D mapping system would help."

And so, I deployed a highly sophisticated three-dimensional (3D) electroanatomical (EAM) mapping system that sped her successful ablation. She was relieved. That is until the bill arrived and the 3D EAM mapping was denied by her insurance carrier.

***

On December 19, 2012, I

wrote about the insurance denial for this case. I was surprised that a denial for payment was made for a portion of a ventricular tachycardia (VT) ablation procedure that was commonplace in my field: three-dimensional (3D) electroanatomic mapping. Worse, I was even more surprised that the denial came from an unknown physician who lacked training in my field and appeared to be nothing more than a foot-soldier of a Cigna insurance company medical coverage policy. Such a denial had never happened to one of my patients before.

Since that blog post was written many months ago, my administrative staff and I have been enduring the appeal. Here's how it's gone.

Shortly after my piece was published, I was notified that someone at Cigna had called our hospital and inquired if they were aware of my blog post. They were. My workplace has graciously permitted me to have this blog since 2005, provided I clearly state the views in that blog are my own, which they are.

Second, I learned that the individual who sent the original coverage denial letter to me was not our local Cigna "regional" medical director. After my post was published, my local medical director from Cigna wanted to talk and explain the proper way that claim denials should handled. A telephone conference was arranged between myself and my the medical director (a local pediatrician from a local academic center which will go un-named) along with another non-medical representative of the local regional office of Cigna. I offered them the opportunity to publish a rebuttal to my post at this site if they desired, but they declined the offer. Instead, I was asked to contact them via e-mail or phone before going public with my concerns about their decision on a blog - "we have a

set way of handling disagreements with policy decisions" I was told. Was this because Cigna's leadership didn't want the bad press or was it a polite way of saying "cease and desist?" I wasn't sure.

So, in the interest obtaining a reversal of my patient's claim denial as easily as possible, I complied. I sent them my first rebuttal in writing and communicated with them via email as requested. My rebuttal went something like this:

Cigna's original denial letter, dated 1 March 2012 stated:

"Use of an intracardiac electrophysiological 3-dimensional mapping system in the diagnosis, treatment, or management of ventricular arrhythmias or any other condition because there is insufficient scientific evidence to support its use does not meet Cigna guidelines for coverage because it is considered experimental, investigational, and/or unproven (E/I/U)."

Cigna's 2012-2013 Medical Coverage Policy regarding 3D electroanatomic mapping systems for VT ablation (which I have copied on my own server, lest it disappear) stated:

The authors state, "although not yet established as requisite or "core" equipment for the EP laboratory, these and other emerging technologies have had, and will continue to have, a major impact on the practice of cardiac arrhythmia management. It is also anticipated that additional new technologies will be developed at ever faster rates in the future" (Tracy, et al., 2006). There has been no update to this statement since 2006.

Baloney. The

EHRA/HRS Expert Consensus statement on VT ablation was subsequently published in in 2009 and that document specifically addresses the use of 3D EAM for VT ablation. It said:

Technological advances have been critical to the development of the field and will continue to play an important role in improving outcomes. The evaluation of new technologies has generally been based on uncontrolled series. There is limited head-to-head comparison of different technologies. Although new technologies generally increase the cost of a procedure when they are introduced, the costs may be justified if they improve outcomes.

...

The focal VT origin can be identified from activation and/or pace mapping.4,381,385,410 Systematic point-by-point activation mapping is the initial preferred technique.233,234,385,409 Some investigators use three-dimensional EAM systems to assist in relating the anatomy to the mapping data.4,124,125,233,381,385,428–430

Surely they wouldn't deny this claim made before that time given this information, right?

Wrong.

Two MORE submissions for higher-order reviews and over four months later, the verdict was handed down: my patient had exhausted all avenues of appeal for the claim. The insurance company would not pay this portion of my patient's bill, no matter what.

Parsing Truths

When deciding what therapies are effective for our field, who should set the requirements for the level of evidence required to determine effectiveness of any therapy, EP societies or the insurance industry? While it is true that prospective randomized trials comparing mapping techniques head-to-head for localizing ventricular arrhythmias have not been done, we should also understand that such a study will never be performed. Why? First, who would pay for such a study to be conducted? The utility of 3D mapping for SVT has been demonstrated and proven effective, in large part because of the greater safety (and greater likelihood of obtaining FDA approval) when supraventricular rhythms are studied compared to ventricular arrhythmias. Second, because the occurrence of the arrhythmia (in this case RVOT VT) is relatively rare, a compelling reason for industry (or government) to fund such a study doesn't exist.

But like SVT ablation, there are three real advantages to these 3D mapping systems for VT ablation that has been repeatedly demonstrated in the literature: (1) catheters can be

returned to prior locations accurately whether the arrhythmia is occurring in a location or not, (2) real reductions in fluoroscopy times can be

achieved and (3) certain 3D EAM systems that use mathematical algorithms (

non-contact balloon mapping) can localize the origin of an arrhythmia using a single heart beat. For the rare patient (like mine) that has infrequent arrhythmias, how would a randomized trial be constructed in hopes of proving the utility of such a technology over conventional mapping by point-to-point techniques? Would such a trial be even ethical to conduct? So, just because a prospective trial has not been performed to demonstrate the utility of a technology in rare circumstances, does this mean electrophysiologists should never utilize such a technology to achieve a successful ablation outcome when other means fail even though such a technology has been shown to be effective in single-center studies? According to Cigna's policy statement, the answer to this question is "yes."

Too bad insurers never have to speak with patients when an ablation fails.

One Last Try

Because I did not want to take "no" for an answer, I asked my administrative staff to see if they could obtain the name of the Cigna "external" reviewer. We had been assured that the case was externally reviewed by an electrophysiologist. We were given the name of an individual but were surprised to find that the physician was a paid employee of Cigna with credentials as an internist and general cardiologist with a nuclear medicine background. To me, it seemed

Cigna "external" review was actually an "internal" review performed by a paid employee of different regional office of Cigna (hence "external" to our region) who was a general cardiologist, not a cardiac electrophysiologist.

I brought this concern to the attention of my local medical director of Cigna by e-mail. In that email I also expressed my concerns about the long time each review had taken. I asked him to examine both issues, since I felt my patient had not received a fair and unbiased claim review. Also, while my patient had received a final denial letter, I never received a notification of their final determination for coverage. After some delay, the director promised to look into my concerns and contacted me by phone later in the week as promised.

In our subsequent discussion, it appeared the director felt the timeliness of their reviews was satisfactory, despite a timeline that stretched over fourteen months for this entire process. In regards to my concerns over who reviewed my patient's claim denial, he claimed there were two "internal" Cigna reviewers and reviewers "external" to Cigna who supported the denial. Of the external reviewers, the director claimed one was board-certified in internal medicine and interventional cardiology and the other external reviewer was board-certified in internal medicine, cardiology and cardiac electrophysiology. He refused to disclose either of the external reviewers' names. When asked, the director stated that the electrophysiologist was in active practice. I reiterated that I still felt the

EHRA/HRS Expert Consensus statement suggested the 3D-mapping falls well within the standard of care. Surely they should reconsider. But despite my pleas for reconsideration, no reversal was forthcoming.

I hung up the phone.

Amazingly, there is little else I can do for my patient's insurance payment denial now. Here I am, a non-anonymous board-certified cardiac electrophysiologist with over twenty years experience who was caught in a challenging case with my patient and am now being told by a pediatrician from an insurance company that there's no merit to my concerns about an unfair denial for coverage of the 3D mapping portion of my patient's claim. I am dumbfounded, confused, and heartbroken for my patient.

So what have I learned?

1) In Cigna's case, some insurance coverage decisions disregard current standards of care and up-to-date expert consensus statements in lieu of poorly-updated corporate medical coverage policies.

2) Specific challenges I encountered with my patient's RVOT VT ablation case had no bearing on Cigna's decision.

3) Physician reviewers often do not hold expertise in the specialty areas they are asked to review. Because they are first and foremost paid employees of the insurer, they turn to corporate medical coverage directives for guidance, even though they are woefully lag current medical practice. As health care dollars get tighter and medicine becomes increasingly codified, significant conflicts of interest will continue to rise for a fair and impartial review of payment denials.

4) If the insurance company claims to have an individual of the same specialty externally review a case, physician providers are not notified of the basis for the denial nor given the names of the reviewers, limiting one's ability to verify the reviewer's credentials or to understand the rationale for the denial. As a result, there is no transparency to the process, nor opportunity for learning or system improvement. To me, this practice should not be condoned. Health care requires continuous quality improvement. More importantly, health care requires trust of all those who touch the field, especially when the care provided, no matter how seemingly far removed, impacts a patient's physical or socioeconomic well-being.

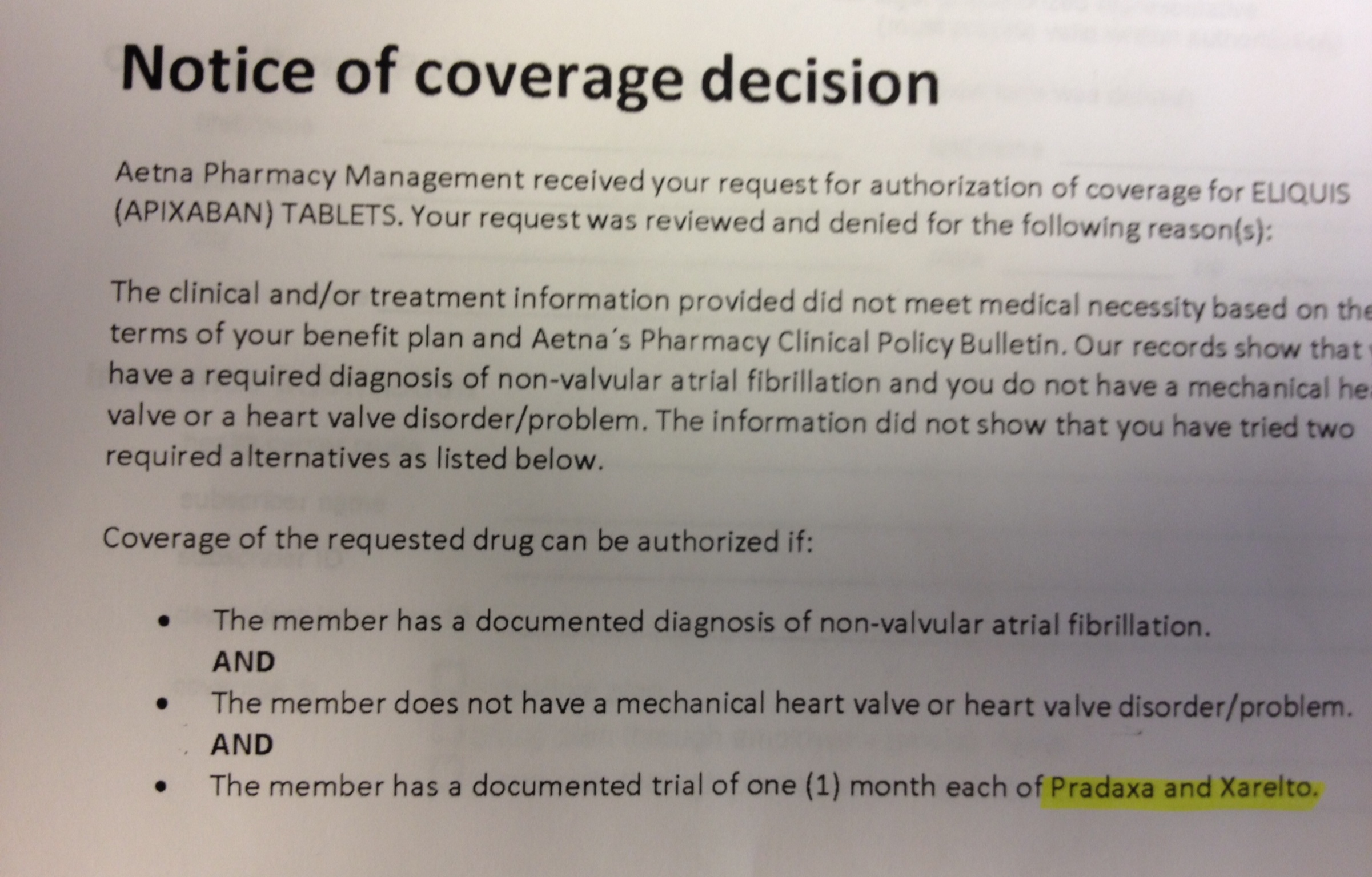

5) Cardiac electrophysiologists should be aware that both Cigna (

here) and Aetna insurance companies (

here) in Illinois now have coverage policies that may opt to deny payment for three-dimensional electroanatomic mapping for VT ablation because they claim they are experimental procedures for this indication based on their outdated internal review of the literature.

6) When confronted about the obsolete nature of their medical coverage policy, Cigna refused to take this into consideration and still refused to overturn by patient's payment denial. Instead, the medical director only promised to include the EHRA/HRS document I sent them in their next annual review of their corporate medical coverage policy for 3D mapping scheduled for 2013-2014.

7) There are technologies that have certain niche benefits for patients, but because they are not "proven" beneficial by randomized trials, in some cases they are no longer be paid for by insurers.

8) My patient will now has four months from the date of her final denial letter to ask for an state-directed independent external review of the Cigna's coverage decision via the

Illinois Insurance Fairness Act as her only remaining avenue for recourse.

So now what?

As I reflect on this case, I used this sophisticated mapping technology because I felt I needed it to improve my patient's outcome and safety. I wonder what this denial of coverage does to the relationship with my patient. Has trust been eroded? As I look forward, how I will perform my next RVOT VT ablation? What do I say to the next patient with a similar arrhythmia? Should I warn all my future patients requiring VT ablation that some of the technology we routinely use to expedite their procedure might not be paid for by their insurer because of a paucity of prospective randomized trials exist (and never will)? Will I have to avoid the use of this technology knowing my patient may have to pay for it because a pediatrician or a general cardiologist who knows nothing about my field might not approve its use? Can I afford to devote this amount of time for wrestling future insurance payment denials that surface?

These are not minor concerns.

So there's the current status of this long, arduous months-long insurance denial review process for just one patient, critically reviewed. It would be easy to make this post a screed against one insurer, and while I have to say that the way this claim denial process was handled was poor at best, we should recall that other insurers have similar policies. It is in the interest of insurers to make the payment denial/review process as difficult as possible for patients and providers. It is also in insurers' best interest to keep out-of-date medical coverage policies in place that consider new technologies "experimental." Better yet, it is even better for insurers to claim niche technologies are "unproven" despite evidence to the contrary and should therefore never be paid. Finally, it is in insurers' best interest to perform internal reviews by uninformed physician reviewers of another subspecialty rather than peer-to-peer independent reviews.

What will it take to change this system?

Maybe we should start with the truth.

-Wes