Based on public record, it appears they have repeatedly misrepresented the date and location of origin of the ABIM Foundation on Internal Revenue Service Form 990 tax forms since at least fiscal year 2009 and did so to shelter multimillion-dollar write-offs for their investment portfolio on the backs of physician testing fees.

{kind=link}

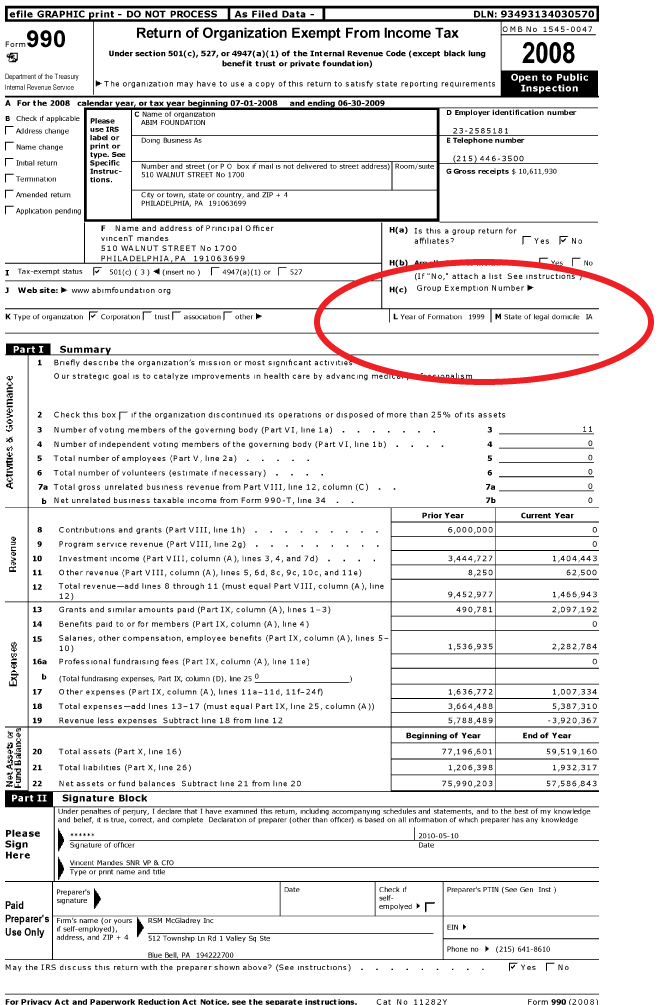

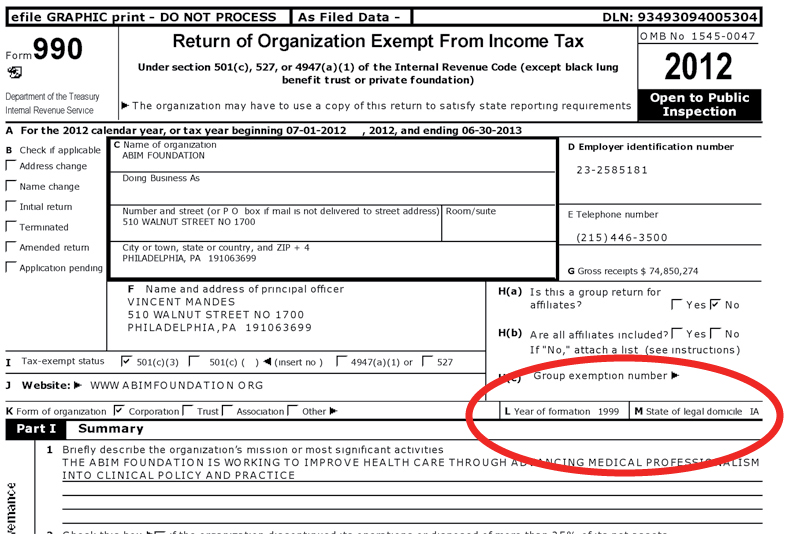

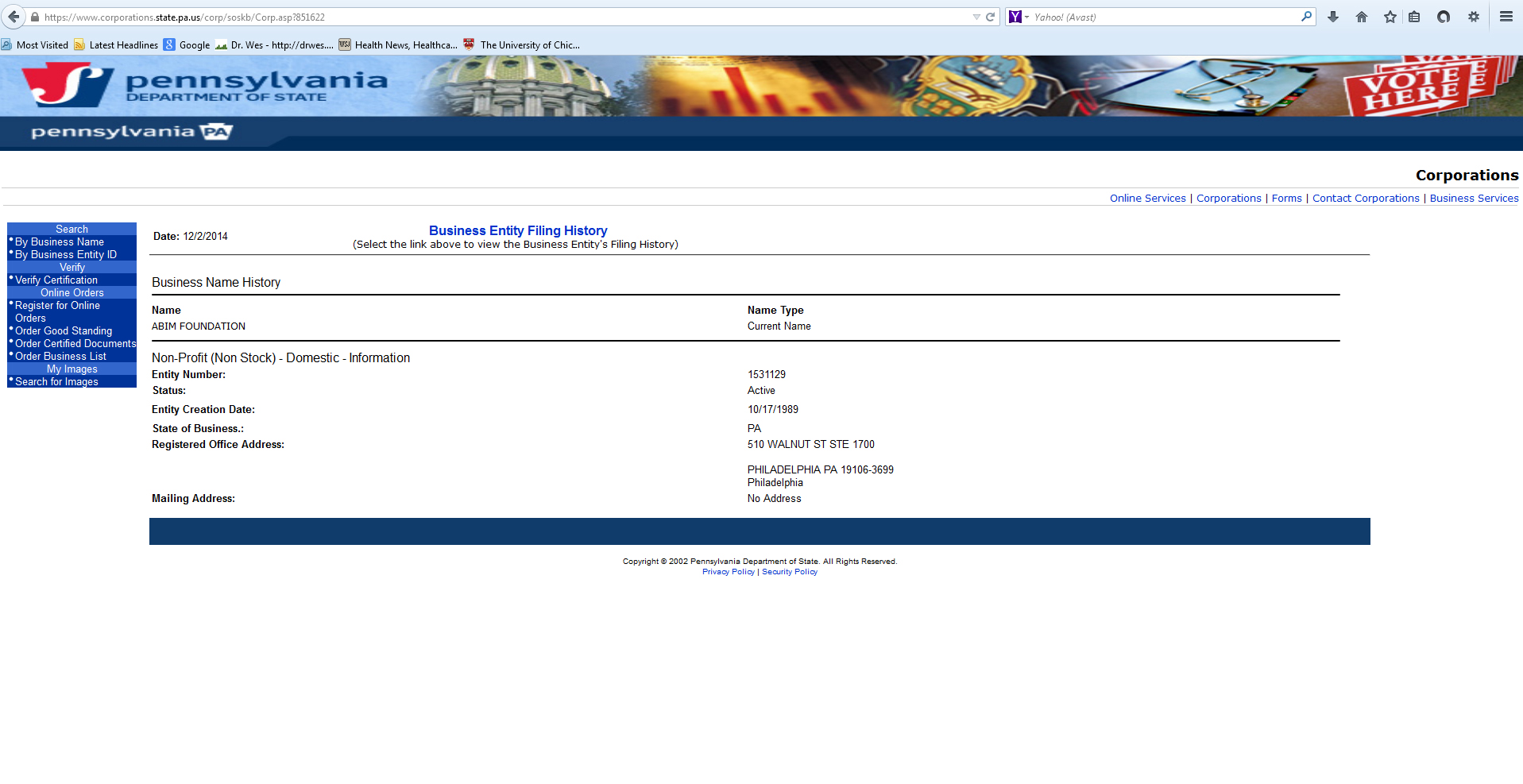

Recall that both recent ABIM Foundation's Form 990's and their website have claimed that the ABIM Foundation was domiciled in Iowa and established in 1999. Recall also, that in my prior research on the ABIM and their Foundation that I asked the current President and CEO, Richard Baron, MD, to explain the discrepancy between the tax form filing information and public record that claims the Foundation was created on 10/17/1989 in Pennsylvania, yet I received no clear explanation for the discrepancy.

{kind=link}

{kind=link}

This date of origination of the ABIM Foundation is important, because if it was created in 1989, the origin of the Foundation would precede 1990, the first year that medical board certification was changed from a life-long designation to a 10-year time-limited status by the American Board of Internal Medicine.

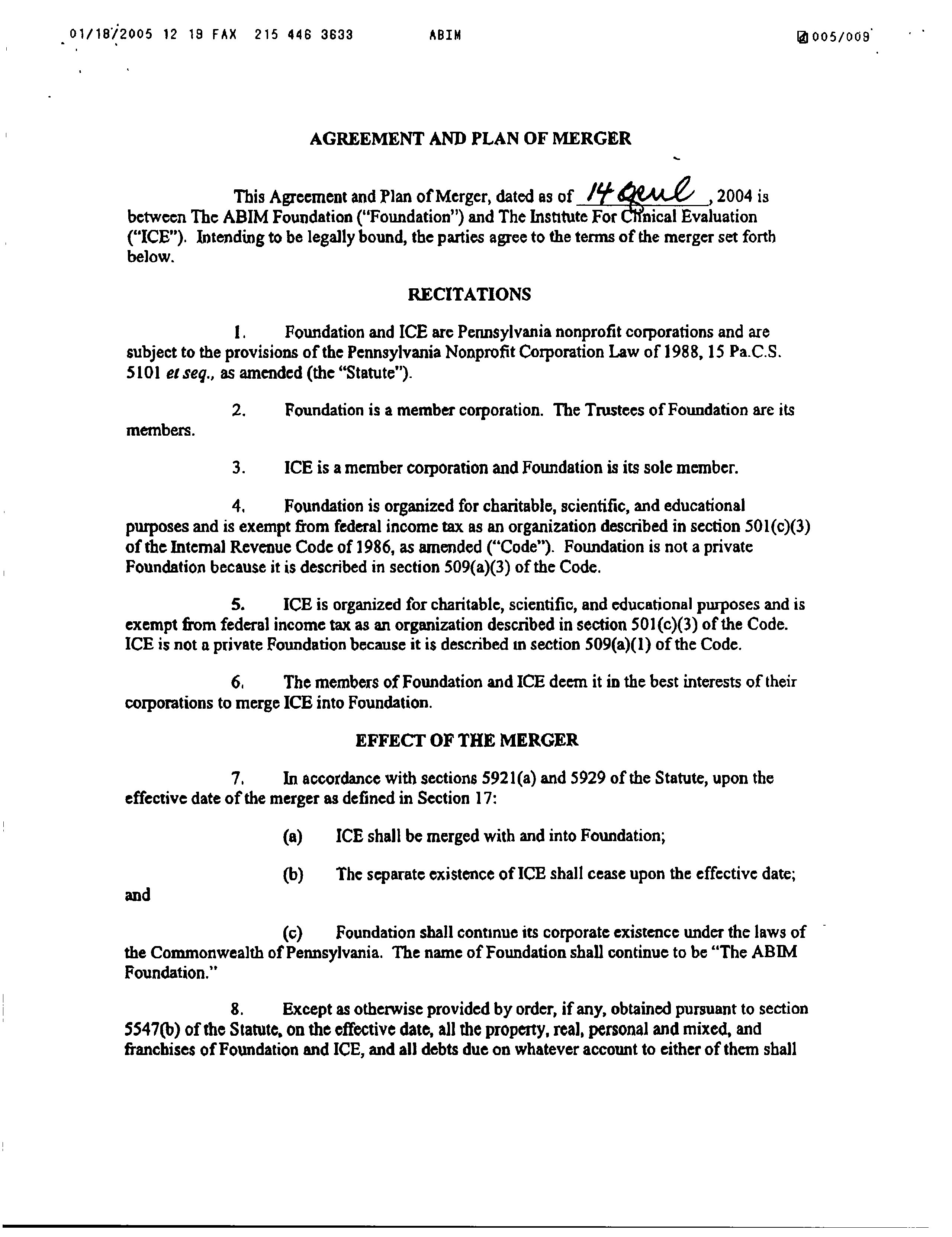

The ABIM Foundation and the Institute for Clinical Evaluation

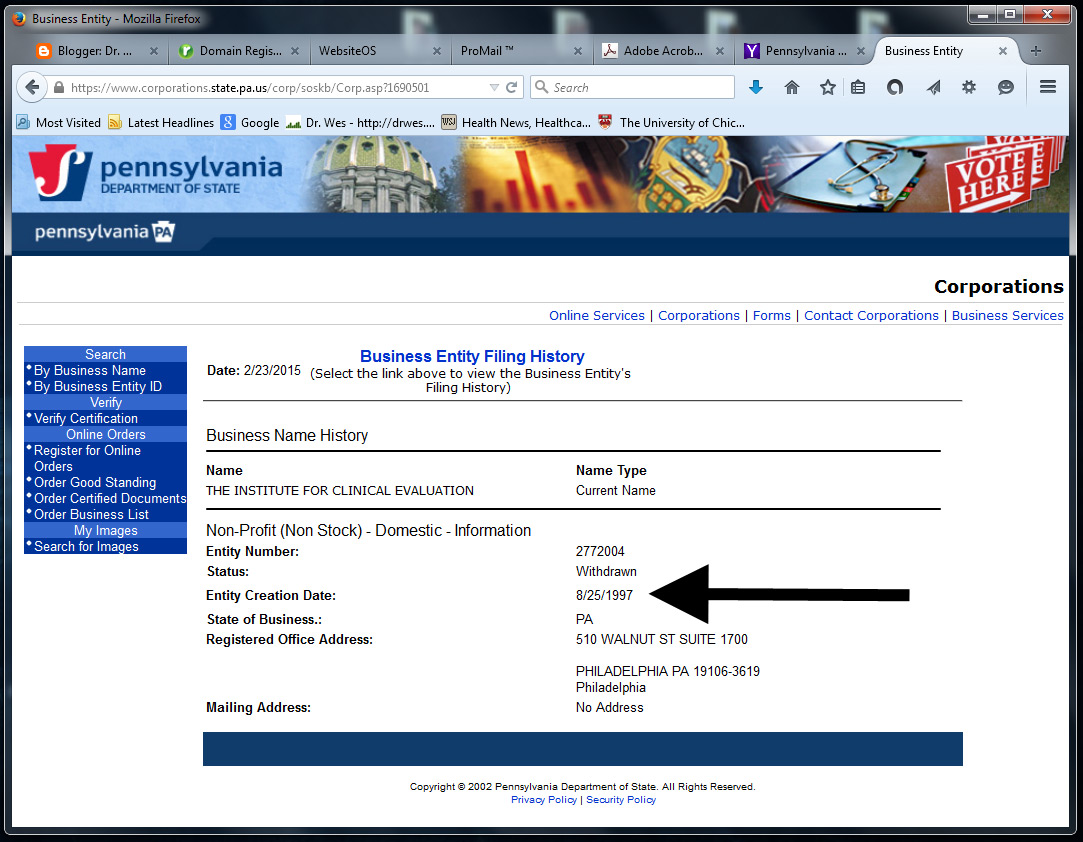

Careful review of the ABIM Foundation's fiscal year 2004 tax forms shows the ABIM Foundation and a separate little-known 501(c)(3) organization, the Institute for Clinical Evaluation (ICE), merged. It appears ICE was created in Pennsylvania in 8/25/1997 by the ABIM Foundation "to assess the usefulness of proficiency testing to the profession."

{kind=link}

{kind=link}

Harry R. Kimball, MACP, the former President of ABIM, was interviewed by Jennifer Wilson of the ACP Internist in 1997, and was quoted as saying:

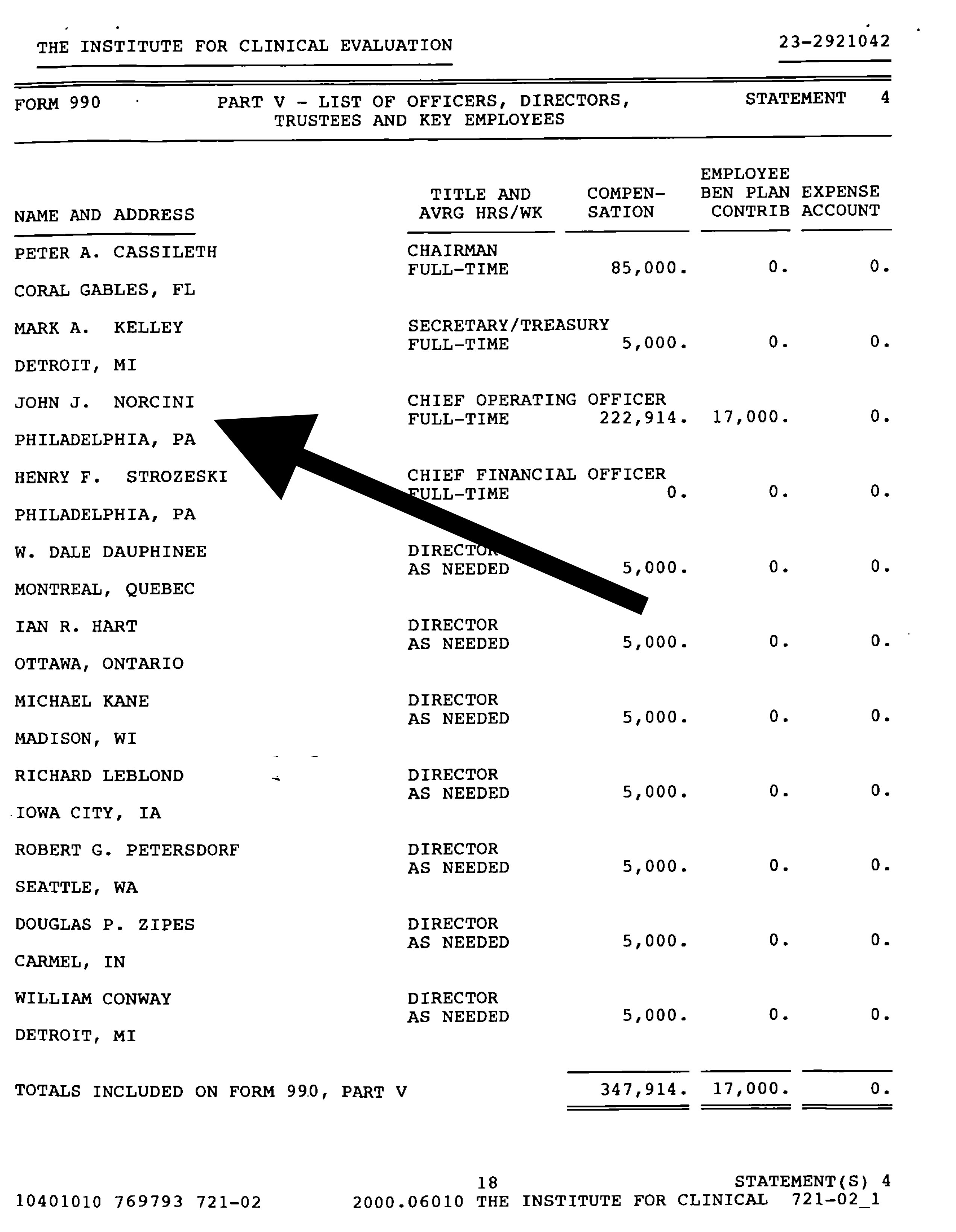

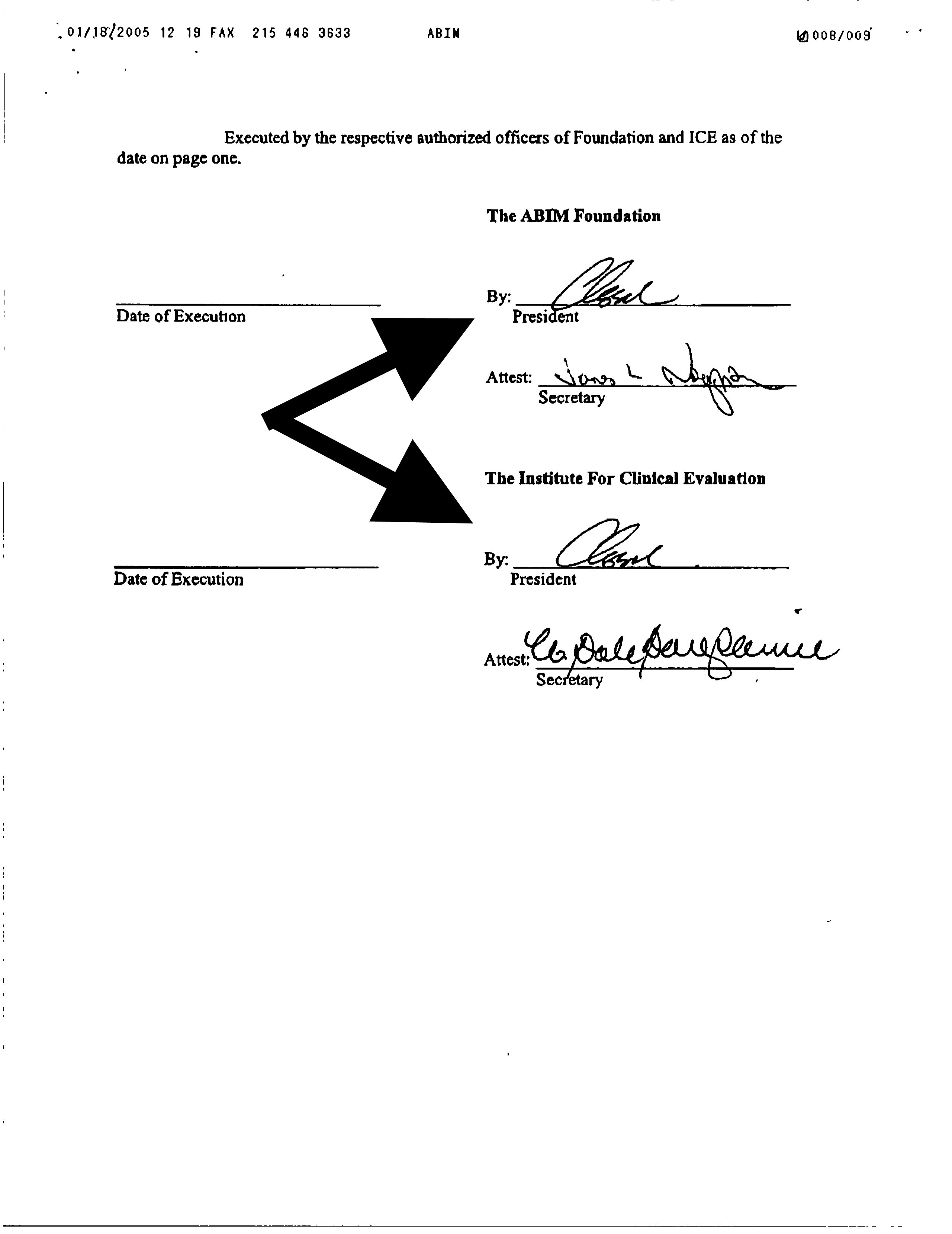

"Several months ago, the ABIM decided to create, through its Foundation, an independent non-profit organization called the Institute for Clinical Evaluation (ICE), which will assess the usefulness of proficiency testing to the profession.But when that organization could not prove such usefulness and spent funds like a drunken sailor to support its non-physician Chief Operating Officer, John J. Norcini, PhD, it appeared the leadership of both organizations later deemed it "in the best interests of their corporations to merge ICE into Foundation." Christine Cassel, MD signed the "Agreement and Plan of Merger" as President of both organizations.

In this context, ICE has the potential to positively influence the development of these standards. At the same time, we can be sure they are compatible with broad-based certification and recertification programs. The Board thinks that ICE can develop collaborative arrangements with professional societies to bundle education and evaluation into a single process. This process would be educationally efficient, credible to patients and acceptable to agencies and institutions responsible for the health and safety of the public.

For the recertification program, the Board is developing a series of practice-assessment modules that allow diplomates to assess their preventive practices, receive feedback from patients and their colleagues about the quality of their professional services and assess the effectiveness efficiency of their clinical practice. The first of these modules is on clinical prevention and will become available this month."

{kind=link}

{kind=link}

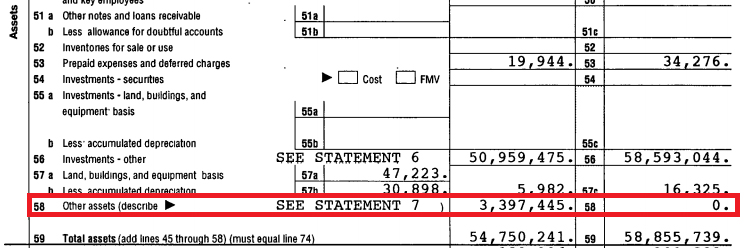

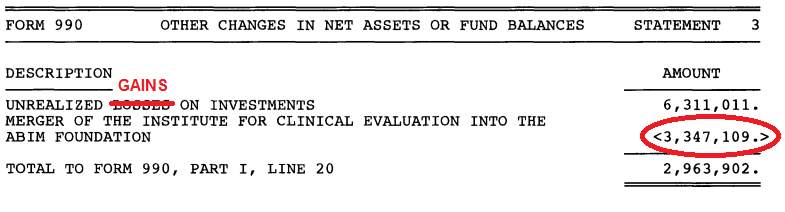

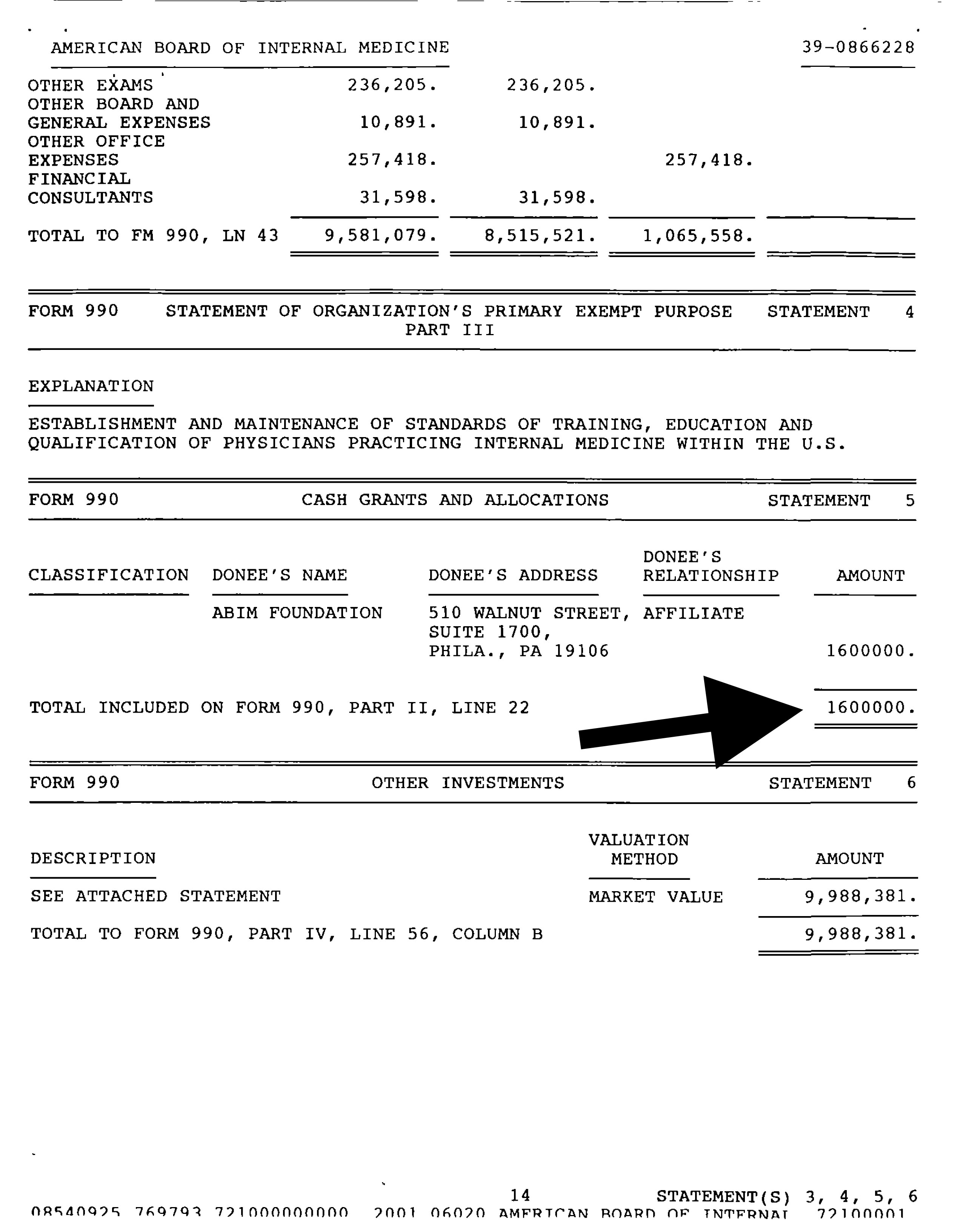

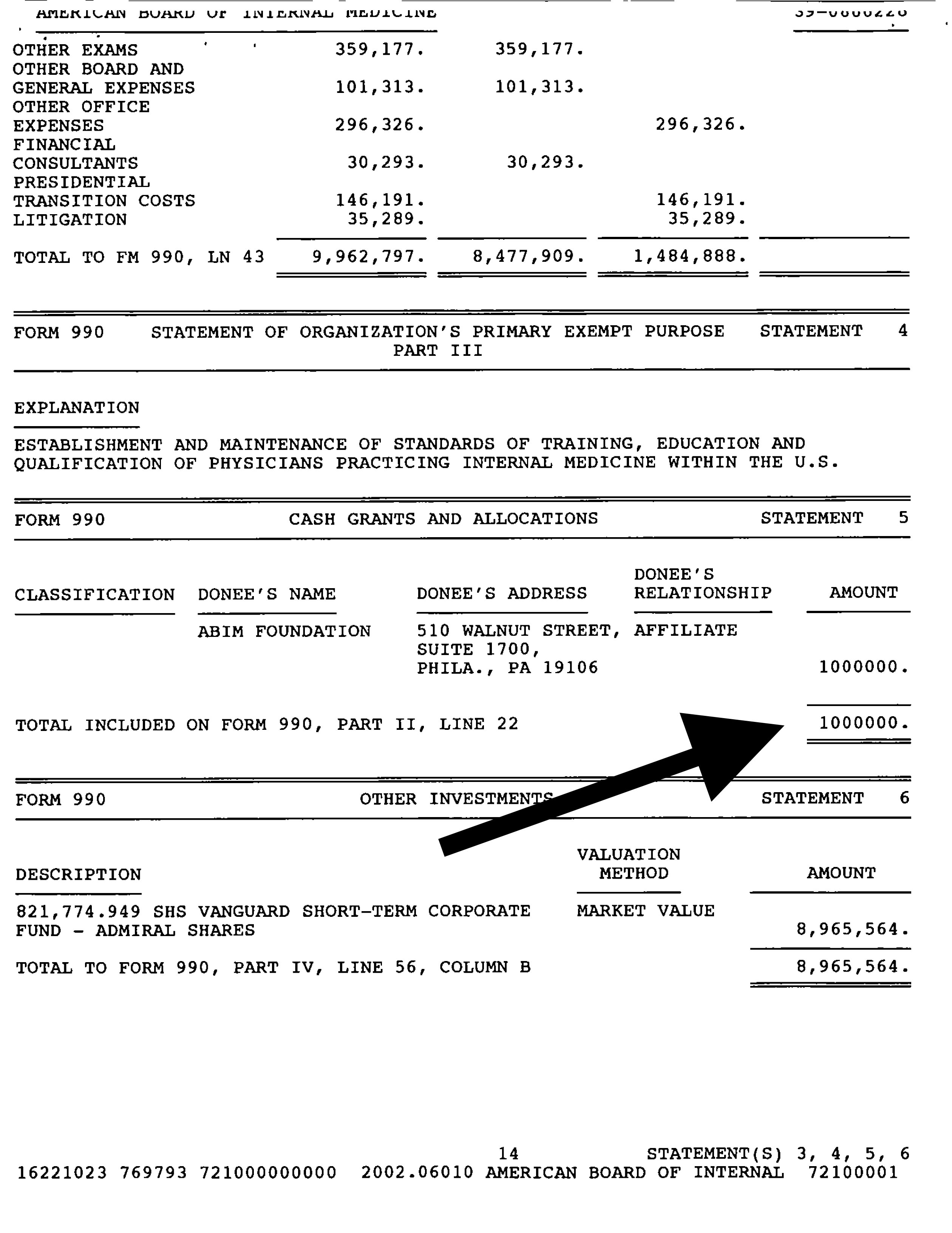

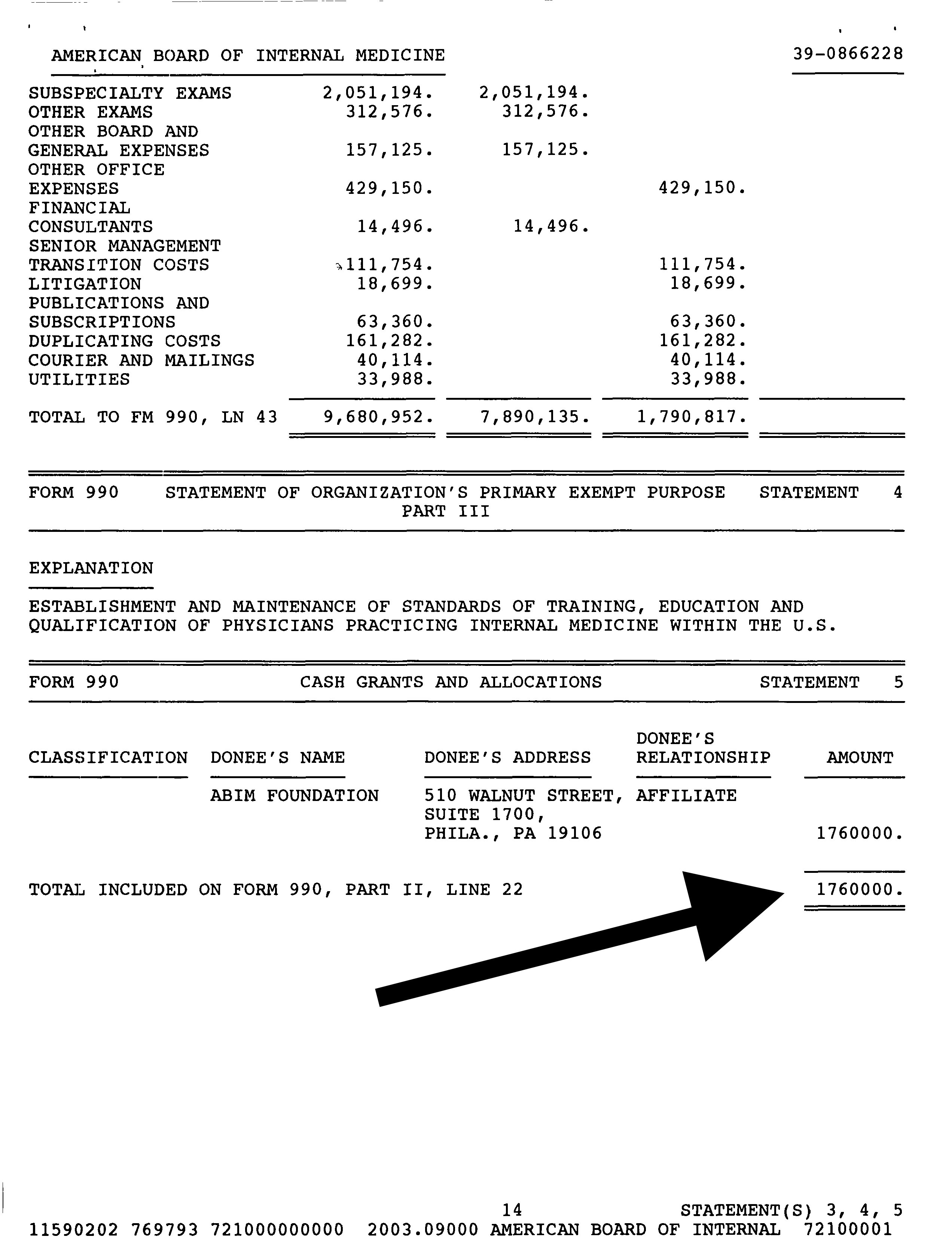

With the merger the ABIM Foundation wrote off a $3,347,109 loss from ICE. It appears that grants were made from the ABIM (who receives 97% of its funds from physician testing fees) to the ABIM Foundation in the three years preceding the merger to handily offset this loss: $1,600,000 in FY 2002, $1,000,000 in FY 2003, and $1,760,000 in FY 2004.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

So what we now know, is that the ABIM Foundation clearly existed before 1999 counter to what its many tax forms and webpage suggest. In my opinion, this misrepresentation on their tax forms and webpage was not just a simple mistake, but was used as a cover-up to the physician community and the public (and perhaps the IRS?) of a $3.3 million dollar loss so they could avoid ridicule over their lack of proof of the value of their testing program while continuing to justify their high salaries and ever-higher testing fees while simultaneously leaving the multimillion dollar investment portfolio held by the ABIM Foundation untouched.

-Wes

Related:

The ABIM Foundation, Choosing Wisely, and the $2.3 Million Condominium

The ABIM Pleads for Mercy

6 comments:

Where will all of this insanity in financial reporting end? Unhappily for ABIM, there is no audit time limit if the IRS can assert that fraud has taken place.

Wes, thank you for your diligence. It is my hope that all the ABMS folks will come clean, if only to avoid the embarrassment that can only emerge as this sort of foolishness comes to light with the other boards. You rock, sir!

Is it possible that this is the equivalent of taking down Al Capone under tax evasion rather than racketeering charges?

If the ABIM gets it right, they will hire you and Charles Cutler, MD as the Czars for their new Department of Pubic Responsibility and Transparency. Keep up the great work !!!

Can any of these expensive and time consuming impositions on physicians, costs of which must be born by patients either in dollars or time, do any better to protect patient safety than Angie's List? I ask this in all seriousness!

IRS form 13909 needs to be submitted on this issue.http://www.irs.gov/pub/irs-pdf/f13909.pdf

Post a Comment